Korea’s shipbuilding industry traces its roots to the early 1970s, a period when the government was pushing hard to transition from a light-in-dustry economy to a heavy-industry one, with concentrated support for heavy chemical industries including shipbuilding, automobiles and petrochemicals. Under the slogan “Build the Nation Through Shipbuilding,” the government institutionalized policy support through shipyard construction, equipment investment and the establishment of naval architecture departments at universities to train top talent.

While the government laid this institutional groundwork, neither the state nor private companies had deep pockets at the time. In some cases, companies had secured land but lacked the funds to build shipyards, securing orders before facilities were even built.

The industry sailed smoothly through the 1980s as growing global trade volumes drove demand for vessels. It went through a period of rapid growth in the 1990s and reached its peak in the early 2000s, coinciding with Korea’s full-scale recovery from the International Monetary Fund (IMF) financial crisis. At that point, Korea topped all three major global shipbuilding competitiveness indicators—ship completions, new orders and order backlog—and held that position for over a decade. Every research and statistical body, from Clarkson Research to Korean and international institutions, recognized Korea as the world’s leading shipbuilding nation. Prior to Korea, Japan had held that title from the 1950s through the 1990s, and before that it was the United States and the United Kingdom.

Then, in the 2010s, Korea’s shipbuilding industry hit a plateau. The primary causes were a drop in new vessel orders due to the global financial crisis and mounting pressure from the rapidly expanding shipbuilding capacity of a major competitor. From the 2020s onward, however, the industry began recovering across all key metrics and entered a new phase of growth. As of 2025, Korea’s ship completions reached 11.26 million CGT (Compensated Gross Tonnage—a standardized unit reflecting vessel weight, cargo capacity, construction complexity and labor input, used as a market share indicator)—the highest figure since the stagnation year of 2016.

How K-shipbuilding Reclaimed

the World’s Top Spot

Shipbuilding Industry

Jeonnam Regional Bureau Chief, Electronic Times

Korea’s shipbuilding industry has staged a remarkable comeback. After holding the world’s top position for two decades, it faltered a decade ago during the global economic crisis and amid intensifying price competition from other countries. Today, however, K-shipbuilding has evolved into a fundamentally different industry. How did it first rise to global leadership? What defines its competitive edge today, and what lies ahead?

The Origins and Growth of Korea’s Shipbuilding Industry

Why Is Korea’s Shipbuilding Industry So Strong?

The driving force behind Korea’s shipbuilding success is high productivity built on innovative construction methods. Building large ships takes time. Techniques like block construction—fabricating a ship in sections and assembling them—and land-based building with sea launch were pioneered by Korea, dramatically boosting productivity. By analogy with fashion, Korea moved the industry from bespoke tailoring to ready-to-wear manufacturing.

These innovations translated directly into competitiveness in high-value-added shipbuilding. Ultra-large container ships capable of carrying more than 20,000 containers in a single voyage, very large crude carriers (VLCCs) and ultra-large LNG carriers were all vessels only Korea could build, and to this day every record for ultra-large vessel orders has been set by Korean shipbuilders.

The rapid adoption and application of ICT has also driven productivity gains. Enterprise resource planning (ERP) systems and integrated CAD software have improved shipyard operational efficiency, while energy-saving systems, optimal route detection systems and other advanced software installed aboard vessels have boosted customer satisfaction. Korea refers to these advances as Smart Ships and Smart Shipyards.

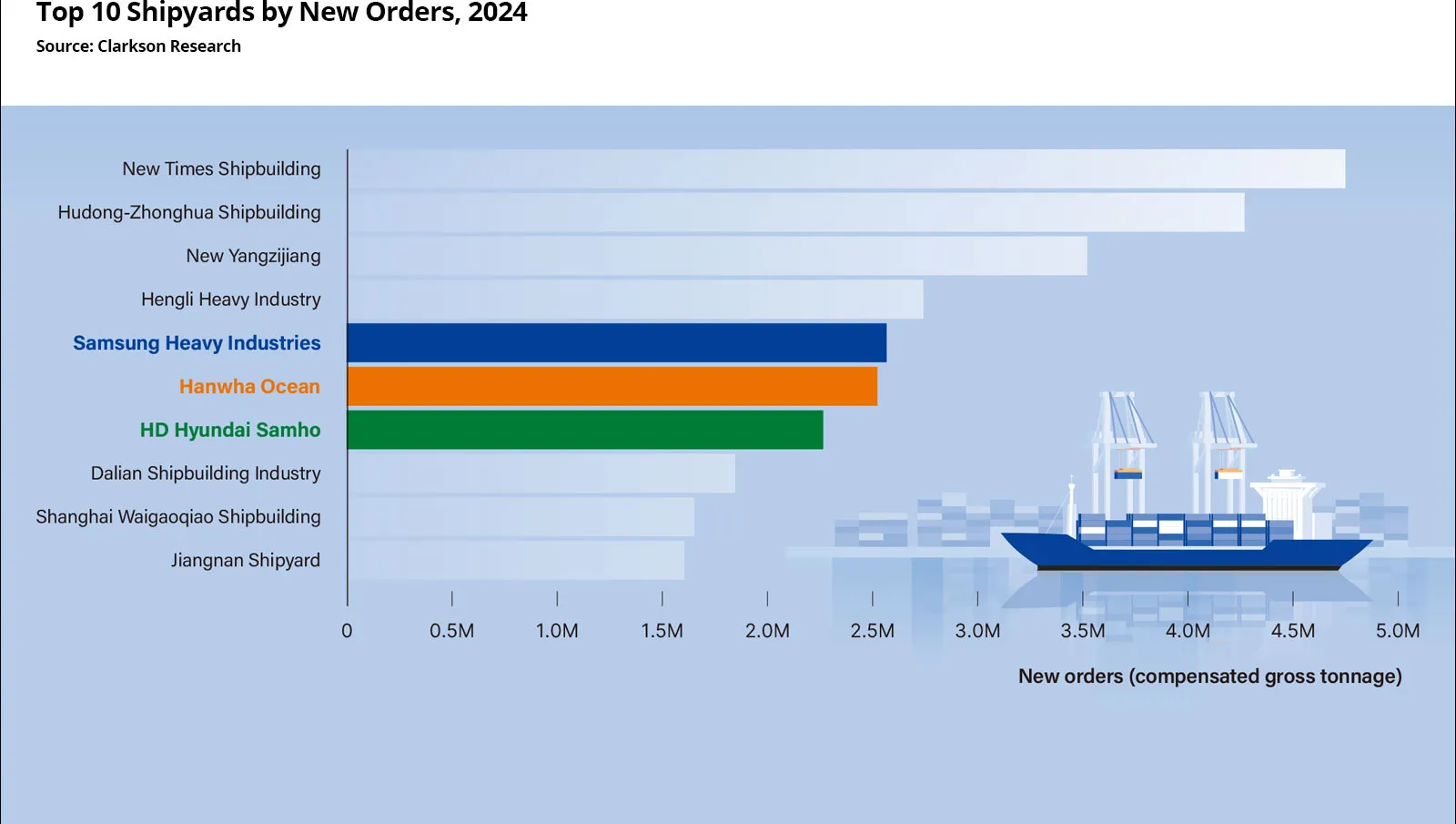

According to Clarkson Research data released earlier this year, total global new ship orders for 2025 reached 56.43 million CGT across 2,036 vessels. By country, China leads at 35.37 million CGT (1,421 vessels, 63%), with Korea second at 11.60 million CGT (247 vessels, 21%). Order backlogs as of the end of January 2026 stood at 180.35 million CGT globally, with China again leading at approximately 111.91 million CGT (61%), Korea at 36.31 million CGT (20%), and Japan in third at 14.82 million CGT (9%).

In CGT volume and vessel count, China holds a commanding lead. But convert those figures to dollar value, and the picture changes entirely. Korea ranks first with an estimated USD 23–25 billion in orders, China comes in at USD 20–24.5 billion, and Japan trails at USD 3–4 billion. Korea orders roughly one-third the CGT and one-fifth the vessels of China, yet its dollar value is higher—a direct result of Korea’s overwhelming dominance in high-value-added vessels such as ultra-large container ships and LNG carriers. This is a clear illustration of how Korea’s competitive edge today lies in quality over quantity.

Korea’s Big Three shipbuilders—HD Korea Shipbuilding & Offshore Engineering, Samsung Heavy Industries and Hanwha Ocean—posted combined operating profits approaching a record 6 trillion won for 2025, all attributable to their shared strategy of pursuing differentiated orders centered on high-value vessel types.

K-shipbuilding: Present and Future

K-shipbuilding is a collective term for Korea’s high-quality ships and shipbuilding technologies that the global market craves.

HD Korea Shipbuilding & Offshore Engineering recently announced plans to develop a 271,000-cubic-meter LNG carrier—twice the capacity of current commercial LNG carriers. The company also unveiled plans for small-to-medium 30,000-cubic-meter LNG carriers: customized bunkering vessels designed to supply LNG directly to specific ships on demand. Development of biofuel-capable vessels is also underway. All of these represent the next generation of premium ships K-shipbuilding is pursuing.

The defining issues in today’s global shipbuilding market are economic efficiency and environmental sustainability. For ships, economic efficiency means maximizing range on minimum energy—which aligns naturally with environmental goals. For shipyards, it means improving construction efficiency. On the environmental side, reducing carbon emissions is the central objective, with the International Maritime Organization (IMO) and European Union (EU) steadily tightening fuel use regulations.

K-shipbuilding’s response strategy is to develop and lead the market for eco-friendly autonomous vessels. These ships use electric propulsion and autonomously identify optimal routes—addressing both economic and environmental goals simultaneously, making them a focal point for every shipbuilding nation. The Korean government, under the banner of securing a decisive technological lead for K-shipbuilding, has been ramping up R&D investment in eco-friendly autonomous ships. In 2025 alone, approximately KRW 260 billion was invested in eco-friendly ship development, digital transformation of shipbuilding processes and autonomous vessel technology.

As AI sweeps across every industry worldwide, the development of digitally integrated eco-friendly ships combining AI and big data is also a defining feature of K-shipbuilding’s direction.

Korean industry, across every sector, has always emphasized a sense of urgency. Under the motto “crisis is opportunity,” companies have looked for technologies to leapfrog competitors when catching up, and for ways to outpace challengers once in the lead. The shipbuilding industry is no different. Innovative construction methods accelerated the pace of catch-up, and once at the top, a strategy of focus and specialization concentrated efforts on high-value-added vessels. That is the foundation on which K-shipbuilding was built.

Today, K-shipbuilding has set sail toward a new goal: beyond high-value-added ships, toward vessels so exclusive and technically demanding that only Korea can build them.